Level:

Graduate

Instructors:

Prof. David Gamarnik

Premal Shah

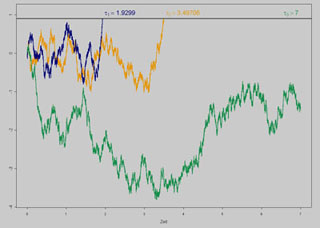

Some stopping times (even hitting times) of Brownian motion. (Image courtesy of Thomas Steiner.)

Course Features

Course Highlights

Course Description

The class covers the analysis and modeling of stochastic processes.

Topics include measure theoretic probability, martingales, filtration,

and stopping theorems, elements of large deviations theory, Brownian

motion and reflected Brownian motion, stochastic integration and Ito

calculus and functional limit theorems. In addition, the class will go

over some applications to finance theory, insurance, queueing and

inventory models.